For decades, control assurance has been dominated by effectiveness testing. Organizations assess whether controls worked as intended over a past period, typically aligned with the annual external audit cycle. This backward-looking approach made sense in a world where assurance was periodic, manual, and audit-driven.

But the way organizations manage risk has evolved. Digital processes, regulatory expectations, and management accountability increasingly demand forward-looking assurance, not just retrospective validation.

To understand this shift, let’s first revisit the full lifecycle of a control.

The Control Lifecycle: Four Interconnected Phases

When examined holistically, control assurance consists of four distinct, but interdependent phases:

- Design & Implementation

- Control Execution

- Effectiveness Testing

- Audit & Assurance

Each phase answers a different assurance question. Together, they determine whether controls genuinely support risk management rather than merely satisfy audit requirements.

Design& Implementation: The Foundation of Any Control

The first phase focuses on design and implementation. This phase assesses whether a control is capable of mitigating its associated risk and whether it has been properly embedded in the organization.

Two dimensions are assessed separately:

- Design – Is the control logically structured to mitigate the identified risk?

- Implementation – Is the control formally documented, communicated, and put into operation?

This phase is most commonly applied when establishing or updating a control framework. Responsible managers or employees are asked to provide evidence that controls have been implemented as intended. Once successfully assessed, a control can be classified as “implemented.”

From a governance perspective, this phase is non-negotiable: A control that is poorly designed or not implemented can not be meaningfully executed or tested for effectiveness.

A well-executed design and implementation assessment typically answers questions such as:

- Does the control still mitigate the linked risk?

- Is the control described as it is actually performed in practice?

- Does the description meet the standards of a good control definition (the 5 W’s and H)

Typical evidence includes:

- Policy and procedure documentation

- System configurations

- Proof of implementation

- Communication and training materials

Only once this foundation is in place does control execution become meaningful.

Control Execution: Where Assurance Moves into the Business

Control execution refers to the actual performance of a control, by people, systems, or a combination of both, according to its defined frequency and procedure.

Historically, controls were executed, but execution evidence was fragmented. Documentation was scattered across emails, shared drives, local folders, or not retained at all. As a result, management had limited visibility, and assuranceactivities remained labor-intensive.

Today, control execution is increasingly recognized as a first-line responsibility. Managers are accountable not only for risks, but also for ensuring that controls are executed consistently and transparently.

Controls may be:

- Manual

- Semi-automated

- Fully automated

Each brings its own challenges. Decentralized evidence storage makes oversight difficult, particularly for second-line functions assessing operating effectiveness.

A clear best practice has emerged: Centralize control execution and evidence.

Doing so simplifies work for control owners, improves transparency for management, and enables earlier detection of issues, allowing organizations to address weaknesses before they escalate.

Watch the webinar ISO 27001 Control Automation: From Control Execution to Continuous Assurance

Automated Controls: Opportunity Comes with Preconditions

Automated controls, such as IT General Controls (e.g. access management, change management) or application controls(e.g. enforced workflows, mandatory fields), offer significant potential for continuous assurance.

However, automation alone does not guarantee reliable evidence.

In practice, organizations often encounter barriers such as:

- Limited data availability – Control data cannot be easily extracted from source systems

- Data quality issues – Incomplete or inconsistent data undermines reliability

- Insufficient logging and monitoring – Common in legacy environments

- Weak control descriptions – Lack of standardization creates misalignment between expected and actual evidence

Without addressing these prerequisites, continuous control monitoring remains aspirational rather than achievable.

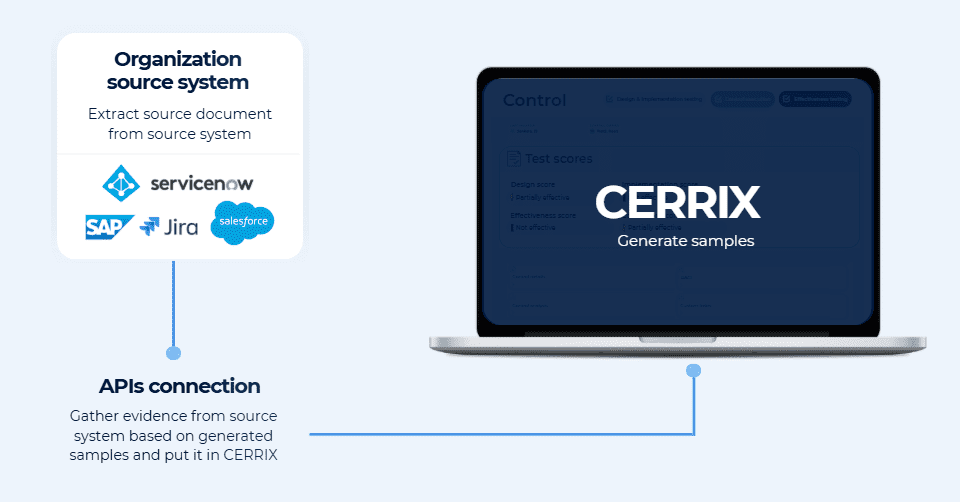

To support this, CERRIX introduced Execution-Based Control Testing. Automated controls can expose their execution results via the Control Execution API, allowing near-real-time capture of execution data directly from source systems. These execution records are then reused for effectiveness testing through automated sampling and review workflows, without relying on screenshots or manually prepared population files.

By linking automated executions directly to effectiveness testing, CERRIX enables continuous insight into control operation while preserving audit trails and expert judgement. Automation therefore strengthens assurance reliability rather than merely accelerating testing activities.

Effectiveness Testing: Still Relevant, but No Longer Sufficient

Effectiveness testing remains the most familiar phase of control assurance. Traditionally, assurance programs relied heavily on periodic tests that looked back over a defined period, mirroring the approach of internal and external audits.

Effectiveness testing answers a critical question: Did the control actually work?

But this assessment is only meaningful if:

- Control execution is properly documented

- Evidence is reliable, complete, and traceable

Modern approaches increasingly support automated effectiveness testing, including:

- Sampling based on execution data

- Direct links to source systems

- Reduced reliance on manual evidence collection

-

This shifts effectiveness testing from a standalone exercise to a natural outcome of structured execution and monitoring.

Audit & Assurance

Audit &assurance form the final phase of the control lifecycle and provide independent validation that controls are designed, executed, and operating effectively. This role is typically fulfilled by internal audit, external auditors, or supervisors.

Historically, audit has driven control testing by looking back at a defined period. In a mature control assurance model, this dynamic changes: audit becomes a user of assurance outputs, not the driver of control execution or testing.

When control design, execution, and effectiveness testing are properly embedded and documented, audit can rely on existing evidence. This enables a shift from ad-hoc audit preparation to continuous audit readiness, reduces disruption to the business, and allows audit to focus on judgement, challenge, and improvement rather than reconstruction of evidence.

Audit & assurance therefore act as the closing loop in the control lifecycle, confirming that the organization is not only compliant, but demonstrably in control.

Conclusion: From Control Activities to Continuous Monitoring

Effective control assurance is not about performing more tests, it is about creating confidence through clarity, ownership, and quality.

- Design & Implementation provide the foundation: clean, reliable control frameworks that are clearly defined, consistently applied, and aligned with the risks they are meant to mitigate. Without this hygiene factor, assurance lacks credibility.

- Control Execution brings assurance into the business. By making execution transparent and structured, managers gain direct insight into how controls operate in practice. Control assurance becomes a management instrument, not an audit exercise.

- Effectiveness Testing adds professional judgement. Through expert review of execution data and evidence, organizations gain a cohesive and complete view of control performance, focused on quality, not volume.

Together, these values shift control assurance from a retrospective compliance activity to make it audit readiness day by day, one that supports informed decision-making, strengthens accountability, and builds lasting trust with internal and external stakeholders.

Blog author

Ruben Andeweg (Senior Risk Consultant, CERRIX)

.jpg)

CERRIX vs ServiceNow: GRC software compared across features, pricing, and compliance

CERRIX vs ServiceNow: GRC Software Compared Across Features, Pricing, and Compliance (2026)

.jpg)

AI in GRC: beyond the hype. What actually works at every level of adoption

Key takeaways from the CERRIX panel on AI in GRC, with practitioners from CERRIX, AuditAgent and 8weeks.co sharing what actually works.

.avif)

Top European GRC tools in 2026: An insider's comparison

This blog compares the top GRC platforms available to European organizations in 2026

What Does GRC Look Like in 2030?

By 2030, AI in GRC will automate evidence collection, control monitoring, and routine reporting across all three lines of defense, shifting risk managers from administrative work to strategic advisory roles

The Complete GRC Chain: Connecting Regulatory Change Management, Risk, and Controls in One Platform

The future of Governance, Risk & Compliance (GRC) lies in connecting regulatory change management directly to risks, controls, incidents, actions, and assurance activities in one integrated platform.

Embedding automation into your risk operating model: Where AI fits and how to make It work

This second part focuses on what makes that automated model intelligent. Where AI fits. What it means for risk professionals in practice.

From checkbox to continuous: How to embed automation into your risk operating model

What it means to truly embed automation into the risk operating model: what changes, what stays the same, and what it takes to make it work in practice.

.jpg)

Why CERRIX acquired Ruler, and what it means for the future of GRC

CERRIX acquires Ruler to connect regulatory change with risk management.

%20(1).png)

Why Data Quality Is the Foundation of AI and Automation in GRC

A strategic look at why structured data in a GRC tool is imperative for automation, AI enabled workflows, and real time risk insights.

.jpg)

Internal Control Framework Challenges: Why COSO and ISO 31000 Implementations Struggle in Practice

Why do internal control framework implementations (COSO, ISO 31000) struggle? Explore common challenges in process design, ownership, tooling, and governance

%20(3).jpg)

Control Assurance Explained: How Organizations Move from Control Testing to Continuous Monitoring

Discover how modern control assurance moves beyond periodic testing to continuous monitoring, with clear ownership, automation, and expert opinion.

Incident Management under DORA: What Risk and Compliance Leaders Need to Rethink

Incident Management under DORA: What Risk and Compliance Leaders Need to Rethink

.jpg)

How to Apply ISO 31000 Risk Treatment in Practice: Insights for Risk and Compliance Leaders

A practical recap of CERRIX ISO 31000 risk treatment webinar

%20(1).jpg)

How We Use CERRIX GRC to Manage Our ISMS: ISO 27001 in Practice

We use our own CERRIX GRC software to manage CERRIX’s ISMS, turning compliance into confidence and showing how ISO 27001 can become part of daily business practice.

.jpg)

Why the Three Lines of Defense Model Is Outdated? What Every Board Should Know About the Three Lines Model

Three Lines Model Explained: Why Boards Must Move Beyond 3LOD

.jpg)

What Is ISO 31000 and How Does It Work?

Discover what ISO 31000 is, how it works, and why it’s essential for risk management in 2025. Learn the principles, framework, and how tools like CERRIX help organizations turn ISO 31000 into practice.

.jpg)

How to Write an Incident Report That Stands Up to Audits

Learn how to write incident reports that are clear, evidence-backed, and audit-ready. Includes a template, best practices, and compliance alignment for risk professionals.

.jpg)

How to Implement ISO 31000: Real-Time Risk Decisions with AI‑Enabled Tools

Discover how to move beyond compliance and operationalize ISO 31000 using AI, real-time dashboards, and structured risk assessments. Learn from webinar insights and best practices tailored for financial services and regulated industries.

%20(1).jpg)

What’s Blocking Your ISMS Rollout? 7 Fixable Challenges for Financial Institutions

Discover the 7 biggest blockers in ISMS rollout for financial institutions—and how to solve them. Learn practical strategies to secure buy-in, define scope, streamline controls, and prepare for ISO 27001 certification.

.jpg)

Trends Driving ISMS Adoption in 2025: What Risk & Compliance Leaders Need to Know

Discover the top trends pushing organizations toward ISMS adoption in 2025—from regulatory changes and remote work to threat evolution and AI. Learn what to prioritize to stay ahead in risk and compliance.

%20(1).jpg)

What Is an ISMS? A Practical Guide for Risk & Compliance Leaders in 2025

An Information Security Management System (ISMS) is more than policy—it’s your organization’s shield against evolving threats, regulation, and reputation risk. Discover what ISMS means, how to implement it, and why it matters in 2025.

.jpg)

The Intelligent Future of GRC: How AI is Reshaping Governance, Risk & Compliance in 2025

Explore how AI is transforming GRC in 2025—from predictive insights and automation to ethical oversight. Learn what features matter, what risks to manage.

.jpg)

How Do You Implement an ISMS in Financial Services Without Slowing Down Innovation?

Implementing an ISMS in financial services? Explore a practical, risk-aligned roadmap tailored for banks, fintechs, and insurers to meet ISO 27001, GDPR, and DORA compliance—without compromising agility.

How Do You Build a Robust ISMS Framework Based on ISO 27001?

Learn how to build a robust ISMS framework aligned with ISO 27001. Discover the key components—people, policies, processes, and controls—to strengthen security and achieve compliance.

.jpg)

When to Conduct Risk Assessments: 6 Enterprise-Critical Moments

Learn when to conduct risk assessments—annual, quarterly, after incidents or change—and how CERRIX ensures continuous compliance.

.jpg)

How do you build a system of quality management that works under ISQM 1?

Learn how to build a system of quality management under ISQM 1. Move beyond compliance to an operational model that proves audit quality.

Top GRC Platforms Compared: Risk Assessment Tools for 2025

Discover the top GRC platforms for 2025 with a focus on risk assessment tools.

What Are Risk Scoring Methods for Financial Institutions? [2025 Guide]

From Risk Assessment to Risk Management: Moving Beyond Checklists in 2025

Understand the evolution from risk assessment to strategic risk management in 2025. Learn why leading organizations are embedding risk into decision-making—and how GRC platforms like CERRIX support this shift.

What is risk management? A strategic guide for leaders in 2025

How Audit Firms Embed ISQM into Daily Practice

In our second ISQM webinar, experts from RSM, Grant Thornton, and CERRIX shared practical insights on how audit firms can embed ISQM into the heart of their operations.

.jpg)

What is the maximum fine for GDPR violations?

Discover the maximum fine for GDPR violations: €20 million or 4% of global turnover. Learn the two-tier penalty system, notable examples, and how to prevent costly data protection breaches.

How do you conduct a GDPR compliance assessment?

Learn how to conduct a GDPR compliance assessment with our step-by-step guide covering data mapping, documentation requirements, and 6 common gaps organizations discover. Reduce risks and ensure compliance.

What are the main requirements of GDPR?

Discover the 7 essential GDPR requirements every organization must follow. Learn about data protection principles, individual rights, breach handling, and practical compliance strategies in this comprehensive guide.

%20(2).jpg)

How often should you review third party risks?

Discover how often to review third party risks with our tiered approach: quarterly for high-risk vendors, semi-annually for medium, and annually for low-risk partnerships.

What should be included in a vendor due diligence process?

Discover what a comprehensive vendor due diligence process should include: financial stability assessment, security controls, compliance verification, risk evaluation criteria, and ongoing monitoring frameworks.

How do you assess vendor risk?

Learn how to implement vendor risk assessment in 5 clear steps. Discover essential strategies to protect your organization from third-party threats and ensure regulatory compliance.

What are the main types of supplier risks?

Discover the 5 critical types of supplier risks that threaten your business continuity. Learn effective strategies to identify, assess, and mitigate these vulnerabilities before they impact your operations.

What is a compliance risk assessment?

Discover how to conduct an effective compliance risk assessment to identify regulatory risks, prevent violations, and transform compliance challenges into strategic business advantages.

How do you report compliance violations?

Learn how to report compliance violations effectively through proper channels while protecting your identity. Discover documentation requirements, whistleblower protections, and what happens after you submit a report.

How do you calculate risk probability and impact?

Learn how to calculate risk probability and impact using proven methods. Transform uncertainty into measurable risks for better decision-making and strategic resource allocation.

What is third party risk management?

Learn what third party risk management is, how it protects your organization from external threats, and the steps to implement an effective TPRM program to ensure compliance and security.

What are the benefits of risk management for businesses?

Discover how risk management benefits businesses by protecting financial health, improving decision-making, ensuring compliance, and creating competitive advantages that transform threats into opportunities.

What is a risk register and how do you create one?

Wondering what a risk register is? Learn how to create this essential tool to identify, assess, and manage organizational risks effectively and boost compliance.

How often do ISO certifications need to be renewed?

Wondering about ISO certification renewal? Understand the three-year cycle, annual surveillance audits, and preparation strategies to maintain compliance seamlessly.

What documents are required for ISO 27001 implementation?

Discover the mandatory and recommended documents required for successful ISO 27001 implementation. Learn how to organize, create and maintain effective ISMS documentation that satisfies auditors and enhances security.

Do I need a consultant for ISO certification?

Wondering if you need a consultant for ISO certification? Discover key factors to make the right decision for your organization based on expertise, resources, and certification complexity.

What industries benefit most from ISO certification?

Discover which industries gain the most value from ISO certification. Financial services, technology, healthcare, and manufacturing organizations see superior ROI while enhancing compliance and competitive advantage.

Can a company lose its ISO certification?

Can a company lose its ISO certification? Discover the 8 common reasons, consequences, and prevention strategies to protect your business reputation and investment.

How long does it take to get ISO 9001 certified?

Discover how long ISO 9001 certification takes, from 4-12 months depending on your organization's size and complexity. Learn the key phases, challenges, and ways to accelerate your quality management journey.

What is ISO 27001 and why is it important for businesses?

Discover how ISO 27001 certification protects your business data, builds customer trust, and ensures regulatory compliance in today's high-risk digital landscape. A complete implementation guide.

From Spreadsheets to GRC Software: Why Pension Funds Need a Modern Approach to Risk Management

What to know about GRC software for nis2

Explore how GRC software helps businesses comply with the NIS2 Directive, enhancing cybersecurity and risk management.

Can automation reduce compliance costs?

Explore how automation can reduce compliance costs, enhancing efficiency and ensuring regulatory adherence.

What industries benefit from compliance automation?

Discover which 6 industries benefit most from compliance automation and how it transforms regulatory burdens into strategic advantages through risk reduction and operational efficiency.

How automation streamlines compliance processes

Discover how compliance process automation reduces costs by 40-60% while minimizing errors and risks. Transform manual workflows into strategic advantages for your organization.

Is cybersecurity compliance automation secure?

Discover if cybersecurity compliance automation strengthens or risks your security posture. Learn implementation best practices that enhance protection while simplifying regulatory management.

Does automation reduce compliance risks?

Explore how automation impacts compliance risks, its benefits, limitations, and integration strategies.

Key sectors affected by NIS2 compliance

Explore the impact of NIS2 compliance on key sectors like energy and healthcare, enhancing cybersecurity and data protection.

Are automated compliance tools reliable?

Exploring the reliability of automated compliance tools and their role in cybersecurity.

%20(1)%20(2).jpg)

DORA compliance checklist for beginners

An essential guide for beginners to understand and implement DORA compliance effectively.

Key benefits of adhering to DORA compliance

Explore the key benefits of DORA compliance, enhancing security, efficiency, and regulatory adherence.

NIS2 compliance: top strategies for success

Explore effective strategies for NIS2 compliance to enhance cybersecurity and regulatory adherence.

EU AI Act vs. GDPR: what's the difference?

Explore the key differences and overlaps between the EU AI Act and GDPR, focusing on regulation, impact, and compliance.

Can GRC tools predict compliance risks?

Exploring if GRC tools can predict compliance risks and their role in risk management.

Can a GRC tool adapt to regulatory changes?

Explore if GRC tools can adapt to regulatory changes, covering compliance management and risk assessment.

How does AI governance impact compliance?

Explore the impact of AI governance on compliance, focusing on regulation, ethics, and risk management.

.jpg)

How to prepare for the EU AI Act implementation?

Learn how to prepare for the EU AI Act implementation with practical steps for compliance.

Is your business ready for the EU AI Act?

Explore readiness for the EU AI Act with insights on compliance, challenges, and strategic planning for businesses.

.png)

How does DORA compliance impact financial sectors?

Discover how DORA compliance strengthens financial sectors, enhancing risk management, digital resilience, and regulatory standards.

.jpg)

What is DORA compliance and why does it matter?

Explore DORA compliance, its significance in financial services, and strategies for effective implementation.

DORA compliance vs other regulatory standards

Explore the differences between DORA compliance and other regulatory standards, focusing on financial regulations and cybersecurity.

Can automation improve DORA compliance efforts?

Explore how automation can enhance DORA compliance efforts by streamlining processes and ensuring ongoing monitoring.

How to integrate GRC with existing systems?

Integrating GRC with existing systems enhances compliance, risk management, and efficiency.

Can settlement discipline improve market stability?

Exploring how settlement discipline can enhance market stability, focusing on its benefits and challenges.

Why real-time analytics in GRC are vital

Real-time analytics in GRC is crucial for proactive risk management and continuous compliance monitoring.

Top 10 Features Every GRC Tool Should Have in 2025

Explore essential GRC tool features like integration, risk management, compliance, governance, and customization.

How to prepare your business for CSDR compliance?

Guide to preparing your business for CSDR compliance, covering key strategies, challenges, and technology solutions.

Embedding ISQM 1 into the DNA of Your Audit Firm: A Risk-Based Approach to Quality Management

Discover how to implement ISQM 1 with a risk-based approach. Learn how audit firms can embed quality management into daily operations and governance.

%20(1).avif)

CERRIX User Conference 2025

On March 12, 2025, industry leaders, assurance experts, and CERRIX customers came together for the CERRIX User Conference 2025—a day of knowledge-sharing, insightful discussions, and collaboration on the future of risk management, compliance, and AI-driven GRC solutions.

From Spreadsheets to GRC Software: Why Pension Funds Need a Modern Approach to Risk Management

CERRIX and BR1GHT Strengthen Long-term Partnership to Enhance Governance, Risk, Compliance and Audit Solutions

Implementing DORA: From Compliance to Long-Term Resilience